Introduction: Why Gen Z Needs a First Salary Budget Template

You just landed your first real job. Your first paycheck hits your bank account — and suddenly you realize nobody actually taught you what to do with it. The rent is due, the student loan servicer is emailing, and somehow your bank balance is already lower than you expected just two weeks in.

You are not alone. The numbers paint a stark picture for Gen Z entering the workforce in 2026:

The paycheck-to-paycheck trap is not inevitable — it is almost always the result of having no system, not a low income. A $52,000 salary, managed with intention, can fund an emergency fund, pay down student loans, start a Roth IRA, AND leave room for travel and fun. This guide shows you exactly how.

The free budget template included in this guide is built specifically for Gen Z first-jobbers. It handles the realities of your financial life that generic budget templates ignore: irregular gig income, subscription stacking, income-based student loan repayment, and the pressure to invest early while managing debt. It is pre-built in Google Sheets, fully customizable, and takes about 20 minutes to set up. For additional financial literacy foundations, the National Endowment for Financial Education (NEFE) and Jump$tart Coalition offer free research-backed programs for young adults.

Understanding Your First Salary Breakdown (Taxes Take 22–28%)

The number on your offer letter is not what lands in your bank account. This catches almost every first-time salaried employee off guard. A $52,000 gross salary typically results in approximately $39,000 in annual take-home pay — or roughly $3,250 per month — after federal income tax, state income tax (varies), Social Security (6.2%), and Medicare (1.45%) deductions.

Here is what the deductions look like on a $52,000 gross salary for a single filer with standard deductions in a moderate-tax state:

| Deduction Type | Annual Amount | Monthly Impact | Notes |

|---|---|---|---|

| Federal income tax | ~$4,440 | ~$370 | 22% bracket starts at $47,150 single 2025 |

| Social Security (6.2%) | $3,224 | $269 | Fixed rate — no negotiation |

| Medicare (1.45%) | $754 | $63 | Fixed rate — no negotiation |

| State income tax (avg) | ~$2,080 | ~$173 | Varies widely — 0% to 13% |

| Health insurance premium | ~$1,200 | ~$100 | Employer-sponsored — pre-tax benefit |

| Total deductions | ~$11,698 | ~$975 | 22.5% effective deduction rate |

| Take-home pay | ~$40,302 | ~$3,359 | Your actual spending/saving power |

2026 Federal Tax Brackets for Single Filers Under 25

| Taxable Income Range | Tax Rate | Tax on This Bracket | Common For |

|---|---|---|---|

| $0 – $11,925 | 10% | $1,192 | Part-time / gig-only earners |

| $11,926 – $48,475 | 12% | Up to $4,386 | Most entry-level salaries |

| $48,476 – $103,350 | 22% | On amount above $48,475 | $50K-$65K first jobs |

| Standard deduction 2025 | $14,600 single — reduces your taxable income significantly | ||

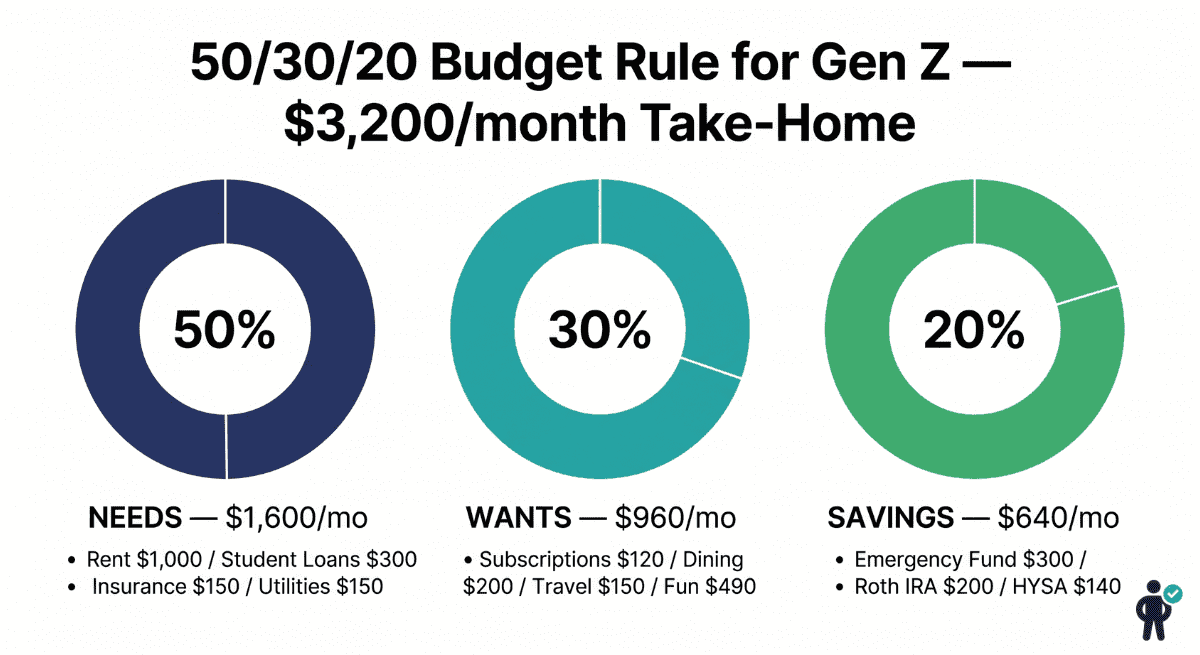

The 50/30/20 Rule Customized for Gen Z First Jobs

The 50/30/20 rule is the most widely recommended budgeting framework for beginners — but the standard version assumes a budget with no student loans, no subscription stacking, and no side hustle income. Here is the Gen Z-adjusted version for a $3,200 monthly take-home:

50% Needs ($1,600/month): Everything required to live and work. Rent is your largest line item — in most mid-size cities a shared apartment keeps this to $800–$1,000. Student loan minimum payments count as a need. Health insurance, renters insurance, and essential utilities round out this category.

30% Wants ($960/month): Everything that improves your quality of life but is not strictly necessary. This includes dining out, subscriptions (Netflix, Spotify, gym), travel, clothing, and entertainment. The key word is intentional — spending freely within this envelope without guilt, but tracking so you know when it is full.

20% Savings ($640/month): Split across three buckets: emergency fund (until 3 months of expenses saved), Roth IRA contributions ($200/month = $2,400/year toward the $7,000 annual limit), and high-yield savings for medium-term goals. Even $640/month consistently invested and saved will build transformative financial security by 30.

Gen Z First Salary Budget Template Walkthrough (12 Categories)

The free template covers every category that matters in your first year of full-time employment. Here is a walkthrough of each section:

Template Link + How to Customize (Google Sheets / Excel / Notion)

Automatic Calculations (Tax Withholding, Net Pay, Savings Rate)

The template automatically calculates: your estimated monthly net pay based on gross salary and filing status, your current savings rate as a percentage of take-home, remaining budget after all categories, and a year-end projection showing where you will be in 12 months if you maintain your current plan. No manual math required.

Automated Google Sheets Freebie: Zero-Based Budgeting + 50/30/20 Formulas

The Google Sheets template comes pre-loaded with two powerful budgeting systems built into the formulas — zero-based budgeting and the 50/30/20 rule. You do not need to understand spreadsheet formulas to use them. Just enter your numbers and the sheet does the math instantly.

Net Income - Fixed Expenses - Variable Expenses - Savings - Debt Payments = $0

Every dollar is assigned a purpose. The template’s “Budget Check” cell highlights green when your allocations equal exactly $0 remaining (balanced) and red when dollars are unassigned or overspent. This ensures no money slips through the cracks.

How the Zero-Based Formula Works in Your Sheet

In cell B2, enter your monthly net (take-home) income. The template then sums all category allocations and subtracts them from B2. The formula in the “Remaining” cell is:

=B2 - SUM(B5:B8) - SUM(B11:B16) - SUM(B19:B21) - SUM(B24:B25)

Where B5:B8 = Fixed expenses (rent, insurance, phone, utilities), B11:B16 = Variable expenses (groceries, dining, transport, subscriptions, personal), B19:B21 = Savings (emergency fund, Roth IRA, HYSA), and B24:B25 = Debt payments (student loans, credit card). When the result is $0, your budget is balanced.

50/30/20 Rule Formulas (Auto-Calculated)

The template includes a “Rule Check” panel that automatically validates your allocations against the 50/30/20 framework. Here are the formulas built into the sheet:

| Category | Formula in Sheet | Target | What It Checks |

|---|---|---|---|

| Needs % | =SUM(Fixed_Expenses)/Net_Income | ≤ 50% | Rent + loans + insurance + utilities + groceries |

| Wants % | =SUM(Variable_Wants)/Net_Income | ≤ 30% | Dining + subscriptions + fun money + shopping |

| Savings % | =SUM(Savings_Debt)/Net_Income | ≥ 20% | Emergency fund + Roth IRA + HYSA + extra debt |

| Balance Check | =Net_Income - Needs - Wants - Savings | = $0 | Zero-based validation (all dollars assigned) |

- Pre-built zero-based budgeting formula — enter income, allocate every dollar, hit $0

- 50/30/20 auto-validator with color-coded pass/fail indicators

- Conditional formatting: cells turn green (on target), amber (close), or red (over budget)

- Monthly rollover tracking — unspent buffer automatically adds to next month’s savings

- 12-month dashboard with savings rate trend line and net worth projection

- Gig income tax set-aside calculator (25–30% auto-reserved)

🏠 Housing (30% Income Max)

Target: $960–$1,000/month. Shared apartments in most cities. Template includes roommate split calculator and rent-to-income ratio checker. Rule: never exceed 30% of gross for rent.

🎓 Student Loans

Target: $200–$400/month. Template includes IBR (Income-Based Repayment) calculator. On $52K, IBR typically sets payments at $230–$290/month. Shows payoff date under different payment scenarios.

📱 Subscriptions

Target: $80–$150/month. Template lists every common subscription with monthly cost so you can audit what you actually use. Average Gen Z spends $219/month — most don’t know it.

🚗 Transportation

Target: $150–$300/month. Public transit vs car payment comparison built in. Car ownership costs $600–$900/month total (payment + insurance + gas + maintenance) — template makes this visible.

🍕 Groceries + Dining

Target: $350/month total. Template splits grocery budget ($200) from dining out ($150) separately — the most important distinction in food budgeting because dining out is the #1 budget leak.

💡 Phone/Internet/Utilities

Target: $120/month combined. Phone $60 (shared plan or budget carrier), internet $40 (split with roommates), utilities $20. Template flags overspend against benchmark automatically.

🛡️ Emergency Fund

Target: $300/month until $9K saved (3 months of $3K expenses). Template tracks progress toward your $9K goal with a visual progress bar and estimated completion date.

📈 Roth IRA / Investing

Target: $200/month minimum. Template includes a compound growth calculator showing your $200/month becomes $1.2M by age 65 at 8% average return. The visual is motivating.

💼 Gig/Side Hustle Income

Target: Track separately. Template has a dedicated gig income tab for Uber, Fiverr, reselling, etc. Automatically calculates estimated quarterly tax payments on gig net income.

💳 Debt Snowball

Target: Extra $50–$100/month above minimums. Template includes debt snowball calculator — list all debts, it auto-ranks by balance and shows exact payoff sequence and dates.

🎉 Fun Money

Target: $200–$400/month guilt-free. Travel, concerts, clothing, hobbies. Template includes a sinking fund for annual expenses (concert tickets, vacation deposits) so they do not wreck your monthly budget.

🔄 Quarterly Review

Template includes a quarterly review tab that compares your budgeted vs actual spending across all 11 categories over 3 months and flags which categories need adjustment.

Sample $52K Salary Budget (Monthly Cash Flow Table)

| Category | Monthly Budget | % of Take-Home | Priority | Notes |

|---|---|---|---|---|

| Rent (shared) | $1,000 | 31% | Needs | 2-bed split = $900-$1,100 in most cities |

| Student loan payment | $280 | 8.7% | Needs | IBR on $52K salary estimate |

| Health/renters insurance | $120 | 3.7% | Needs | Employer plan + renters ~$15/mo |

| Transportation | $200 | 6.2% | Needs | Transit pass or minimal car costs |

| Groceries | $200 | 6.2% | Needs | Meal prep reduces this significantly |

| Phone + utilities | $120 | 3.7% | Needs | Shared plan + split utilities |

| Subscriptions | $100 | 3.1% | Wants | Audit regularly — creep kills budgets |

| Dining out | $150 | 4.6% | Wants | The most common overspend category |

| Fun money / personal | $280 | 8.7% | Wants | Guilt-free within this envelope |

| Emergency fund | $300 | 9.3% | Savings | Until $9K saved — then redirect |

| Roth IRA | $200 | 6.2% | Savings | Auto-invest day 1 of each month |

| High-yield savings | $140 | 4.3% | Savings | Travel fund, car fund, opportunity |

| Total allocated | $3,090 | 95.7% | — | — |

| Monthly buffer | +$209 | 4.3% | Buffer | Rolls to savings if unspent |

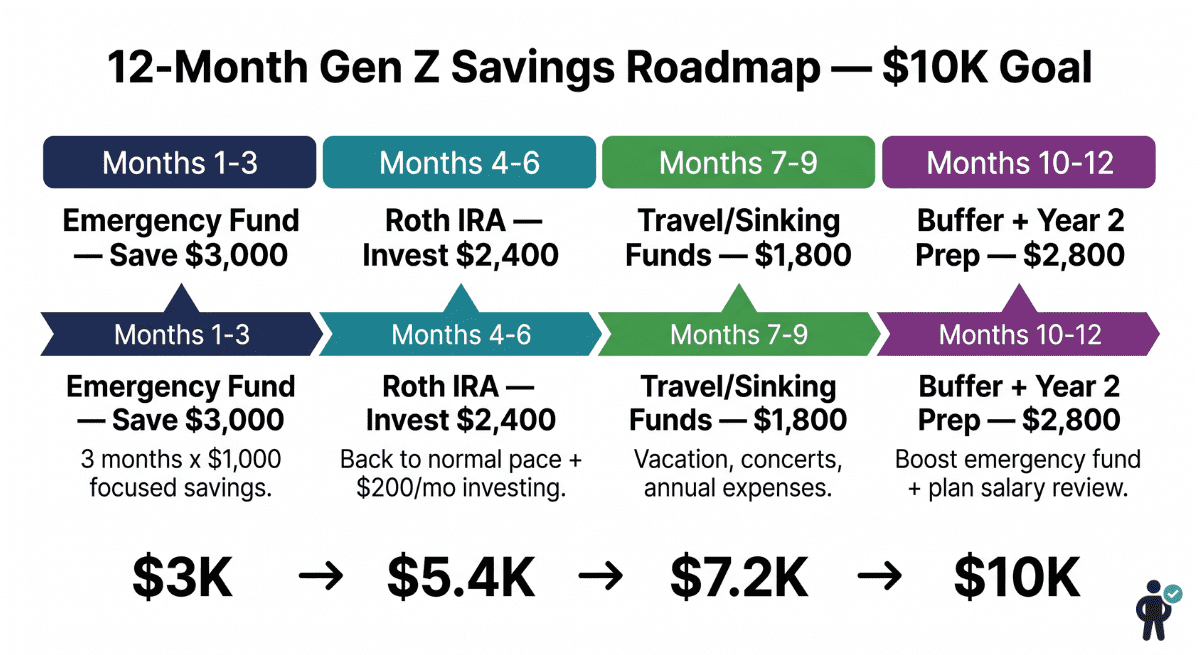

12-Month First Salary Savings Roadmap ($10K Goal)

Emergency Fund Sprint — Target: $3,000

Temporarily boost savings to $1,000/month by cutting fun money to $150 and redirecting your $209 buffer. Reach $3,000 in 3 months — enough for one month of full expenses. This is your financial airbag. Nothing else matters until it exists.

Roth IRA + Normalize — Target: +$2,400

Return to the normal budget plan. Start contributing $200/month to a Roth IRA (Fidelity, Schwab, or Vanguard — all free to open). Add $2,400 to your investments over 3 months. Automate this transfer on the first of each month so it happens before you can spend it.

Travel + Sinking Funds — Target: +$1,800

Build sinking funds for annual expenses that typically derail budgets: a planned vacation ($600), holiday gifts ($400), annual subscriptions ($200), and a car maintenance reserve ($600). These are expenses you know are coming — funding them monthly prevents budget crises.

Buffer + Year 2 Prep — Target: +$2,800

Push emergency fund toward the full $9,000 (3 months of expenses) goal. Evaluate your first year: track your actual spending vs budget, identify your biggest overspend categories, and plan a salary negotiation for Year 2. Starting Year 2 with $10K saved and a clear budget is a genuine financial advantage most of your peers will not have.

Your First 90 Days: Career Finance Guide

The first 90 days at a new job are not just about proving yourself professionally — they are the most consequential financial window of your early career. Decisions you make (or avoid) during onboarding and your first quarter compound for decades. This section covers the three pillars every Gen Z first-jobber should lock in before Day 91.

Pillar 1: Emergency Fund Automation (Starter $1K → 3–6 Month Reserve)

Before investing, before extra debt payments, before anything else — you need a cash buffer between you and life’s inevitable surprises. A car repair, a medical bill, or an unexpected move should not force you onto a credit card at 24% APR.

Phase 1: The $1,000 Starter Fund (Days 1–60)

Your first goal is $1,000 in a high-yield savings account (HYSA) separate from your checking account. At current rates, HYSAs pay 4.5–5.0% APY — your money earns while it waits. Open one at an online bank (Ally, Marcus by Goldman Sachs, or Wealthfront Cash) and set up an automatic transfer of $125/week from your checking account on payday. In 8 weeks you will hit $1,000 without thinking about it.

Phase 2: Build to 3–6 Months of Expenses (Days 60–365)

Once your $1,000 starter fund is in place, maintain automatic transfers but reduce to $300/month (as reflected in the budget template). Your target is 3 months of essential expenses — roughly $5,400–$9,000 depending on your cost of living. For most Gen Z first-jobbers on $52K, aim for $9,000 (3 × $3,000 monthly essentials).

The progression looks like this:

| Timeline | Target Balance | Monthly Contribution | Strategy |

|---|---|---|---|

| Days 1–60 | $1,000 | $500 (aggressive sprint) | Reduce wants to bare minimum temporarily |

| Months 3–6 | $3,000 | $300–$500/month | Resume normal budget; consistent auto-transfer |

| Months 7–12 | $6,000–$9,000 | $300/month + buffer rollover | 3-month reserve complete; redirect excess to Roth IRA |

| Year 2+ | $9,000–$18,000 | Maintenance only | Build toward 6-month reserve as income grows |

Pillar 2: Benefits & Pre-Tax Optimization (Free Money You Must Claim)

Your employer benefits package is the single largest source of “free money” available to you in your first year — and most Gen Z workers leave thousands of dollars on the table by not enrolling correctly during onboarding. Here is exactly what to prioritize:

401(k) Employer Match: The Guaranteed 50–100% Return

If your employer offers a 401(k) match, contribute at least enough to capture the full match from Day 1. A typical match structure is “100% of the first 3% + 50% of the next 2%” — meaning if you contribute 5% of your $52K salary ($2,600/year), your employer adds $2,080. That is an immediate 80% return on your contribution before any market growth.

On a $52K salary with a standard match:

| Your Contribution | Annual Amount | Employer Match | Total Going to Retirement | Your Take-Home Reduction |

|---|---|---|---|---|

| 3% of gross | $1,560 | $1,560 (100% match) | $3,120/year | ~$100/month (pre-tax) |

| 5% of gross | $2,600 | $2,080 (full match) | $4,680/year | ~$167/month (pre-tax) |

| 6% of gross | $3,120 | $2,080 (match maxed) | $5,200/year | ~$200/month (pre-tax) |

HSA (Health Savings Account): The Triple Tax Advantage

If your employer offers a High-Deductible Health Plan (HDHP), you gain access to an HSA — the most tax-advantaged account in the U.S. tax code. HSAs offer triple tax benefits: contributions are pre-tax (reduce your taxable income), growth is tax-free, and withdrawals for qualified medical expenses are tax-free.

For 2025, the individual HSA contribution limit is $4,150. Even contributing $100/month ($1,200/year) builds a medical reserve while reducing your tax bill by $144–$264/year (depending on your bracket). The advanced strategy: pay current medical expenses out-of-pocket, let your HSA invest and grow tax-free for decades, then reimburse yourself in retirement.

FSA (Flexible Spending Account): Use-It-or-Lose-It Pre-Tax Savings

If you do not have an HDHP (and therefore cannot use an HSA), enroll in your employer’s FSA for predictable medical and dependent care costs. The 2025 limit is $3,300 for healthcare FSA. Estimate conservatively — FSA funds generally expire at year-end (some plans offer a $640 rollover or 2.5-month grace period). Good candidates for FSA: contacts/glasses, prescriptions, therapy copays, dental work you know is coming.

Pillar 3: Risk Protection (Term Life + Disability Insurance for Young Adults)

Nobody at 22 wants to think about insurance — but this is precisely when it is cheapest and most important to lock in. Two policies form the foundation of financial protection for young professionals:

Term Life Insurance

Who needs it: Anyone with financial dependents (cosigners on loans, aging parents you support, a partner relying on your income, or anyone who would bear your debts). Even without dependents, locking in a policy at 22–25 guarantees the lowest possible premiums for a 20–30 year term.

How much: Standard recommendation is 10–20x your annual salary. On a $52K salary, a $500,000–$1,000,000 20-year term life policy costs approximately $20–$35/month for a healthy non-smoking 22–25 year old. This is less than a single streaming subscription.

Where to get it: Check if your employer offers group term life (often 1–2x salary free). Supplement with an individual policy from Ladder, Haven Life, or a traditional broker. Individual policies are portable — they follow you when you change jobs.

Disability Insurance (Long-Term)

Why it matters more than life insurance at 22: A 22-year-old is significantly more likely to become disabled than to die during their working years. Long-term disability (LTD) insurance replaces 60–70% of your income if illness or injury prevents you from working for an extended period.

Employer-provided LTD: Many employers offer basic LTD coverage (often 60% of salary) at no cost or low cost. Enroll during onboarding. Check whether the benefit is taxable (employer-paid premiums = taxable benefit; employee-paid = tax-free benefit). If your employer does not offer LTD, or the coverage is limited, supplemental individual policies cost $25–$50/month for young professionals.

- Week 1: Open a HYSA and set up $125/week auto-transfer for starter emergency fund

- Week 1: Enroll in 401(k) at minimum match percentage (typically 5–6%)

- Week 2: Elect HDHP + HSA if healthy, or traditional plan + FSA if you have recurring medical costs

- Week 2: Enroll in employer group life insurance and long-term disability

- Month 2: Get quotes for individual term life policy ($500K, 20-year term)

- Month 3: Confirm emergency fund hit $1,000; begin Roth IRA contributions

Gen Z Budget Killers to Avoid (The 5% Traps)

1. Subscription Creep: The average Gen Z person pays for 12 active subscriptions but regularly uses only 5. At $15–$20 each, the unused ones cost $84–$140/month — $1,680/year vanishing invisibly. The fix is simple: once per quarter, open your bank statements and cancel anything you have not used in 30 days.

2. Lifestyle Inflation: The most dangerous financial moment for first-jobbers is the first salary increase. Behavioral economics shows that most people immediately expand spending to absorb the raise rather than saving the difference. When you get a raise, bank at least 50% of the after-tax increase before adjusting your lifestyle at all.

3. No Expense Tracking: Budgeting without tracking is guessing. You cannot manage what you do not measure. The template solves this — spend 10 minutes every Sunday reviewing the week’s transactions. It takes less time than one episode of Netflix and has an outsized impact on your financial behavior.

4. The All-or-Nothing Mindset: Missing your budget in one category does not mean the entire month is a write-off. The #1 reason budgets fail is that people treat one slip as total failure and abandon the plan entirely. A budget is a framework, not a punishment. Overspend by $40 on dining out and simply note it — do not give up.

5. Ignoring Gig Income Taxes: If you earn any side income and do not set aside 25–30% for taxes, the IRS will collect it all at once in April — often with penalties on top. This single mistake has financially set back thousands of first-year workers. Treat your tax savings as a non-negotiable category, not an afterthought.

Bonus Calculators: Take-Home Pay, Loan Simulator, Savings Rate

The free template includes three bonus calculator tabs beyond the main budget:

Take-Home Pay Calculator: Enter your gross salary, state, filing status, and any pre-tax deductions (401k, HSA, FSA). The calculator outputs your estimated monthly and annual net pay, effective tax rate, and marginal tax bracket. Updated for 2026 federal brackets and standard deduction amounts.

Student Loan Simulator: Enter your loan balance, interest rate, and income. The simulator calculates your standard repayment amount, your Income-Based Repayment (IBR) amount, the total interest paid under each plan, and your payoff date. For most $52K earners with $32K in loans, making minimum IBR payments results in full forgiveness after 20 years — but paying an extra $100/month can eliminate the loan in under 8 years and save $12,000+ in interest.

Savings Rate Calculator: Enter your monthly income and total monthly savings. The calculator shows your current savings rate, projects your net worth at ages 30, 40, 50, and 65 based on current rate, and shows how much each 1% increase in savings rate accelerates your financial independence date.

Budgeting on Irregular Income: Guide for Freelancers & Gig Workers

If your income varies month to month — from freelance projects, gig work (Uber, DoorDash, Fiverr), seasonal employment, or commission-based roles — the standard budget template needs one critical adjustment. You cannot budget based on your best month because it sets unrealistic expectations that collapse during lean periods.

The “Lowest of 3” Rule for Variable Income

The rule: Budget your monthly expenses based on the lowest income of your past 3 months. This ensures your baseline spending plan is always funded, even in a down month. Any income above that floor goes to savings acceleration, debt paydown, or a dedicated “income smoothing” fund.

Budget Base = MIN(Month 1 Income, Month 2 Income, Month 3 Income)

In the Google Sheets template, enter your last 3 months of net income in cells D2:D4. The budget base auto-calculates as =MIN(D2:D4) and feeds into your zero-based allocation. Surplus months (anything above the MIN) auto-routes to your income smoothing fund.

How to Structure a Variable Income Budget

| Income Scenario | Month 1 | Month 2 | Month 3 | Budget Base (MIN) | Action |

|---|---|---|---|---|---|

| Consistent gig | $2,800 | $3,100 | $2,600 | $2,600 | Budget on $2,600; bank surpluses |

| Feast-or-famine | $4,200 | $1,800 | $3,500 | $1,800 | Budget on $1,800; fund 2-month buffer |

| W-2 + side hustle | $3,200 | $3,200 | $3,700 | $3,200 | Budget on W-2 only; gig = bonus savings |

The Income Smoothing Fund

For freelancers and gig workers, the income smoothing fund is a separate HYSA bucket (beyond your emergency fund) that holds 2 months of baseline expenses. When a month’s income exceeds your budget base, the excess flows here. When a month falls short, you draw from this buffer instead of touching your emergency fund or going into debt.

Target balance: 2× your monthly budget base. On a $2,600/month budget base, maintain a $5,200 smoothing fund. This transforms unpredictable income into predictable cash flow for budgeting purposes.

Frequently Asked Questions (FAQ)

Q1: What percentage of first salary should go to rent?

The standard guideline is no more than 30% of gross income — or roughly 28% of take-home pay. On a $52,000 salary that means targeting $1,083/month or less. In expensive cities like New York or San Francisco this is genuinely difficult without roommates. Having one or two roommates is the single highest-impact financial decision most first-jobbers can make — reducing your housing cost from $2,500/month to $1,000–$1,200 frees up $16,000–$18,000/year for savings and debt repayment.

Q2: How much student loan payment on a $50K salary?

Under Income-Based Repayment (IBR), your monthly payment on a $50,000–$55,000 salary is typically $230–$310/month for a $32,000 loan balance at 5.5% interest. This is your federally capped IBR payment — it adjusts annually based on your income. The standard 10-year repayment plan would be approximately $340/month for the same balance. The right choice between plans depends on your loan type, forgiveness eligibility, and whether you plan to work in public service (PSLF reduces payments to 10 years with tax-free forgiveness). The budget template’s loan simulator calculates both scenarios for your specific numbers.

Q3: Should Gen Z invest in a Roth IRA immediately?

Yes — with one condition: build a $1,000 starter emergency fund first (about 2–3 months of focused saving), then start Roth IRA contributions immediately. The Roth IRA’s core advantage is paying taxes now at your current low rate (likely 12–22%) so all future growth is completely tax-free. Every year you delay costs you years of compound growth that cannot be recovered. Even $50/month started at 22 outperforms $200/month started at 30. Open a Roth IRA at Fidelity, Schwab, or Vanguard — all have zero minimum balance requirements and free index funds. Automate a monthly transfer on the first of each month.

Q4: How do I budget for gig income or side hustles?

Treat all gig income with a split system: when any gig payment arrives, immediately transfer 25–30% to a dedicated tax savings account (a separate high-yield savings account labeled “Taxes”), then budget the remaining 70–75% as supplemental income. Never treat gig income as reliable — it is variable and may not recur. Use it for accelerating goals (emergency fund, debt paydown, extra Roth contributions) rather than funding recurring monthly expenses. The budget template’s gig income tab tracks quarterly estimated tax obligations automatically based on your net gig earnings.

Q5: What is a realistic first-year savings goal on a $52K salary?

A realistic and achievable Year 1 savings target on a $52,000 salary is $6,000–$10,000, depending on your city’s cost of living and student loan situation. Following the budget template in this guide, the $52K example accumulates approximately $640/month in formal savings plus a $209 buffer — totaling $849/month or roughly $10,000 over 12 months. This includes $3,600 in emergency fund contributions, $2,400 in Roth IRA contributions, and $3,600 split between high-yield savings and sinking funds. This is not a theoretical number — it is achievable with intentional spending and consistent tracking.

Trusted Financial Literacy Resources for Gen Z

Building financial knowledge is a lifelong process. These nonprofit organizations offer free, evidence-based financial education programs specifically designed for young adults entering the workforce:

- National Endowment for Financial Education (NEFE) — A nonprofit foundation providing free personal finance research, tools, and educator resources. Their programs cover budgeting fundamentals, retirement planning, and debt management with curriculum backed by academic research. Ideal for self-directed learners who want structured financial education without sales pitches.

- Jump$tart Coalition for Personal Financial Literacy — A national coalition of organizations dedicated to advancing financial literacy among students and young adults. Jump$tart maintains the National Standards for K-12 Personal Finance Education and offers a clearinghouse of vetted educational resources, including budgeting worksheets, investment primers, and career finance guides specifically for 18–25 year olds entering the workforce.

Both organizations are nonprofit, accept no product advertising, and provide their materials free of charge. They represent the gold standard for unbiased financial education — a valuable complement to the practical budgeting template in this guide.

📥 Download Your Free Gen Z Budget Template Pack

Everything you need to start your first salary budget today — Google Sheets, Excel, Notion, and a printable PDF version all included free.

Or get the template + monthly budget tips delivered to your inbox:

No spam. Just the template + occasional money tips for first-jobbers. Unsubscribe anytime.