Introduction: Why US Credit Matters for Immigrants (0→670 in 12 Months)

You arrived in the United States with skills, savings, and ambition — but no US credit score. Landlords reject your apartment applications before you can explain yourself. Car dealerships quote absurd interest rates. Banks turn you away for basic credit cards. This is the invisible wall every new immigrant faces, and it has nothing to do with your financial responsibility back home.

The good news: the path from zero to a 650+ FICO score is now faster and more accessible than it has ever been. In 2026, ITIN holders can access secured credit cards, rent reporting services, and free credit-boosting tools that simply didn’t exist five years ago — and we’ve mapped out the exact 12-month sequence that works.

Step 1: Check Your Starting Point (ITIN vs SSN Credit Barriers)

Most new immigrants are what the credit industry calls “credit invisible” — you have no US credit file at all, which is different from having bad credit. Lenders see a blank file and default to the worst-case assumption. Here is exactly what is happening and what you can do about it immediately.

If you have a Social Security Number (SSN), you can apply for most standard credit products on day one. If you only have an Individual Taxpayer Identification Number (ITIN) — issued by the IRS to non-residents and resident aliens — your options are narrower but very real. Several major issuers now explicitly accept ITIN applications in 2026.

VantageScore 4.0 update for 2026: VantageScore now scores consumers with as little as one month of credit history and one account — making it meaningfully easier for recent immigrants to get their first scoreable file. Many apartment landlords use VantageScore, so you may qualify for housing faster than the FICO 8 timeline suggests.

Free Credit Reports for Immigrants (AnnualCreditReport + Alternatives)

Start here before doing anything else:

- AnnualCreditReport.com — official free weekly reports from Experian, Equifax, and TransUnion (since 2023 the free weekly access is permanent)

- Experian.com — free Experian report + FICO score via their app; also reveals if you have any existing file

- Credit Karma — free TransUnion + Equifax reports with VantageScore; works with ITIN and SSN

- Nova Credit — if you have established credit in your home country, initiate a foreign credit import here first

Step 2: Three ITIN-Friendly Secured Credit Cards (No SSN Needed)

Secured cards are the single most important tool for building US credit as an immigrant. You deposit cash ($200–$500 typically) as collateral, receive a card with that limit, use it for everyday purchases, pay it off monthly, and the issuer reports your perfect payment history to the bureaus. Within 6 months, this creates the payment history and account age that push your score from invisible to 580+.

The critical detail: not all secured card issuers accept ITIN. The three below have confirmed ITIN acceptance as of 2026.

- $200 minimum deposit

- 1.5% cash back on all purchases

- No annual fee

- Reports to all 3 bureaus

- Automatic upgrade review at 6 months

- ITIN accepted ✅

- $200 minimum deposit

- 2% cashback at restaurants/gas

- 1% everything else

- No annual fee

- First year cashback matched

- ITIN accepted ✅

- $200+ deposit (you choose limit)

- No credit check required

- $35 annual fee

- Reports to all 3 bureaus

- No bank account needed

- ITIN accepted ✅

#1 Capital One Quicksilver Secured Mastercard ($200 Deposit)

The Capital One Quicksilver Secured is the top recommendation for most immigrants because it combines no annual fee, cash back rewards, and an automatic upgrade path to an unsecured card — all while accepting ITIN applicants. After 6 months of responsible use (paying the full balance monthly, keeping utilization below 30%), Capital One’s system automatically reviews you for a credit line increase and potential upgrade to the unsecured Quicksilver card, which is a major positive event for your credit file.

#2 Discover it Secured ($200 Deposit + 2% Cashback)

Discover is the only major issuer that matches your first year of cashback earnings — effectively doubling every reward you earn in months 1–12. For immigrants who are already spending money on groceries, gas, and food, this makes the Discover it Secured the highest-earning secured card available. Discover also reports to all three bureaus and conducts automatic upgrade reviews after 7 months. Apply at discover.com/credit-cards/secured and indicate ITIN when prompted for a tax ID number.

#3 OpenSky Visa Secured ($200+ Deposit, No Credit Check)

OpenSky is the safest option for immigrants who are concerned about being denied even a secured card. There is no credit check — zero hard inquiries — because the deposit fully collateralizes the card. You don’t even need a US bank account; deposits can be made by money order or Western Union. The $35 annual fee is the trade-off, but for immigrants who are newly arrived and haven’t established a bank account yet, OpenSky removes every possible barrier to entry.

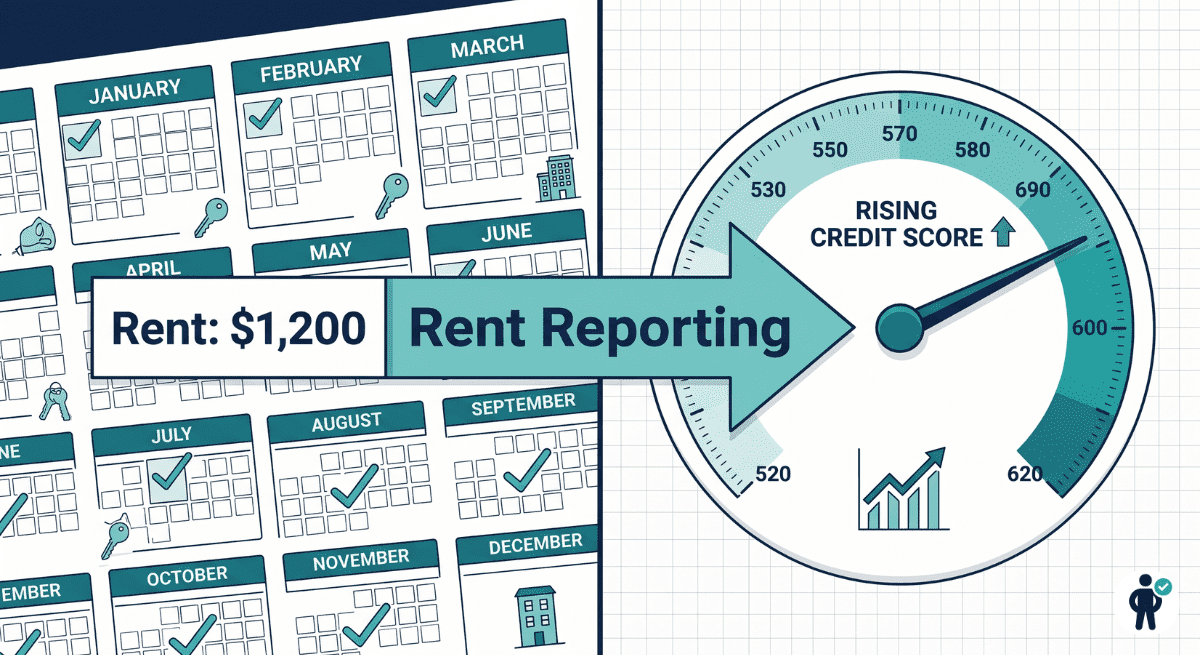

Step 3: Rent Reporting (40% FICO Impact – Biggest Free Boost)

Payment history is the single largest FICO factor — it accounts for 35% of your score. If you’re paying rent every month and that payment isn’t on your credit report, you are leaving your biggest financial asset unreported. Rent reporting services fix this by forwarding your monthly payments to one or more credit bureaus, creating the payment history that credit scores depend on.

In 2026, several states (California, New York, Colorado) now legally require large landlords to offer rent reporting to tenants. But even if your state doesn’t mandate it, these services work independently of your landlord:

- Experian Boost (Free) — Connects to your bank account and reports rent, phone, and utility payments to Experian only. Takes 5 minutes to set up and shows results immediately. Average boost: 10–20 points.

- RentTrack ($6.95/month) — Reports to all three bureaus (Experian, Equifax, TransUnion). Most powerful option because it affects all three bureau scores. Average boost: 25–40 points within 90 days.

- Rental Kharma ($8.95/month) — Retroactively reports up to 2 years of past rent payments, creating instant credit history depth that newer services can’t match.

- Landlord enrollment path — If your landlord uses property management software (AppFolio, Buildium, Rentec Direct), ask them to enable tenant credit reporting — many platforms offer it free to landlords.

Step 4: Credit-Builder Loans + Authorized User Strategy

Credit-builder loans are designed specifically for people with no credit history. The mechanics are reversed from a normal loan: the lender holds the loan amount in a locked savings account while you make monthly payments. When you finish paying, you receive the money — and a 12-month history of perfect loan payments now sits on your credit report. This adds the “installment loan” account type that credit scores reward, diversifying your credit mix.

The second strategy — becoming an authorized user — requires a trusted family member or close friend already in the US with 7+ years of perfect payment history on their card. They add you to their account (you don’t need to use the card or even receive it), and their entire positive history on that card is added to your credit file. This single move can add 50–80 points by instantly aging your credit history.

2026 Best Credit-Builder Apps (Chime, Self, MoneyLion)

- Self (Self Lender) — $25/month builds a $300–$1,700 loan over 12–24 months. Reports to all 3 bureaus. After 3 months, unlock a Self Visa secured card using your saved balance as collateral. ITIN accepted. This is our top pick.

- Chime Credit Builder — No annual fee, no minimum deposit, no hard credit check. Move any amount from your Chime spending account as collateral. Reports to all 3 bureaus. Requires a Chime checking account (free). Excellent for immigrants who want no upfront cost.

- MoneyLion Credit Builder Plus — $19.99/month membership gives access to a $1,000 credit-builder loan. Reports to 3 bureaus. Also includes cash advance access up to $300. Best for immigrants who want additional financial tools alongside credit building.

Step 5: Utility & Phone Reporting (74% See Instant FICO Jump)

If you pay a US phone bill, electric bill, gas bill, or streaming service, Experian Boost can add those payments to your Experian credit file — for free. The service connects to your bank account (or credit card statements), identifies qualifying bill payments going back up to 2 years, and lets you select which ones to add.

According to Experian’s own data, 74% of users who add utility and phone payments see an immediate FICO score increase, with an average jump of 39 points. For credit-invisible immigrants, this is frequently the difference between having no score and having a scoreable 550–580 — enough to begin the rest of the credit-building process.

Which bills qualify for Experian Boost in 2026:

- AT&T, Verizon, T-Mobile, Spectrum phone/internet bills

- Electric, gas, and water utility payments

- Netflix, Disney+, HBO Max, and other streaming services

- Insurance payments (auto, renters)

- Rent payments (if not already reported via a rent reporting service)

Step 6: 12-Month Credit Building Timeline (Proven 0→670 Path)

The sequence matters as much as the individual products. Opening too many accounts at once damages your score through hard inquiries and new account penalties. The timeline below spaces actions optimally to maximize score growth while minimizing setbacks.

Months 1–3: Two Secured Cards + Rent Reporting (Score: 580–620)

Week 1: Pull all three bureau reports at AnnualCreditReport.com. Set up Experian Boost — add phone, utilities, and rent. Week 2: Apply for Capital One Quicksilver Secured (ITIN). Set up Self credit-builder loan at $25/month. Week 3–4: If no bank account, apply for OpenSky Visa Secured. Begin using your secured card for 1–2 small purchases monthly.

First billing cycle closes. Pay the full balance — never carry a balance. Keep utilization at or below 10% for maximum scoring benefit (e.g., if your limit is $200, charge no more than $20). VantageScore becomes scoreable this month for most immigrants — check Credit Karma.

3 months of payment history established. Experian FICO score becomes available. Ask a family member in the US to add you as an authorized user on their oldest card. Expected score range: 580–620 VantageScore, 550–580 FICO 8.

Months 4–6: Upgrade One Card + Credit-Builder (Score: 630–660)

Request a credit limit increase on your Capital One card — this lowers your utilization ratio on that card (same spending, higher limit = lower %). Capital One may grant this without a hard inquiry. Add RentTrack ($6.95/mo) to start reporting rent to all 3 bureaus.

Self credit-builder loan has now established 5 months of on-time installment payments — a significant positive signal. You’re building both revolving (credit cards) and installment (loan) credit types simultaneously. Expected FICO 8: 610–640.

Capital One’s automatic upgrade review fires at 6 months. Many ITIN holders are approved for an unsecured card upgrade at this stage — your deposit is returned and your card converts to a regular Quicksilver. This is a major milestone. Expected score: 630–660 FICO 8.

Months 7–12: Apartment/Car Loan Approved (670+ FICO)

7 months of established history. Discover’s automatic upgrade review begins. Score stabilizes in the 650–670 range. You are now in range for most apartment applications, many auto lenders, and some unsecured credit cards.

Consider applying for a starter unsecured card — the Petal 2 Visa or Deserve EDU Mastercard both accept ITIN holders and have no annual fees. Adding a third line of credit diversifies your mix further.

Self loan completes — your savings are returned and you now have a 12-month perfect installment loan history. With all pieces in place (2–3 cards, rent reporting, utilities, installment loan), most immigrants hit 670–690 FICO 8 by month 12. Mortgage pre-approval territory begins at 680.

2026 Credit Building Products Comparison Table

| Product | Monthly Cost | FICO Impact | ITIN Accepted | Time to Results | Best For |

|---|---|---|---|---|---|

| Capital One Quicksilver Secured | $0/mo + $200 deposit | High (payment history + utilization) | ✅ Yes | 3–6 months | Primary card, upgrade path |

| Discover it Secured | $0/mo + $200 deposit | High + cashback rewards | ✅ Yes | 3–7 months | Best rewards + upgrade |

| OpenSky Visa Secured | $35/yr + $200+ deposit | High (all 3 bureaus) | ✅ Yes, no bank needed | 1–3 months | No credit check, no bank acct |

| Experian Boost | Free | Moderate (Experian only) | ✅ Yes | Instant (same day) | Rent + utilities on Experian |

| RentTrack | $6.95/mo | High (all 3 bureaus) | ✅ Yes | 30–90 days | Maximum rent reporting impact |

| Self Credit Builder Loan | $25/mo | High (installment history) | ✅ Yes | 3–6 months | Credit mix + forced savings |

| Chime Credit Builder | $0/mo (Chime acct required) | Moderate–High | ✅ Yes | 3–6 months | No minimum deposit path |

| Nova Credit | Free (per application) | Very High (imports existing history) | ✅ Yes | Immediate (existing history) | Immigrants from 15+ countries |

| MoneyLion Credit Builder+ | $19.99/mo | Moderate–High | ✅ Yes | 3–6 months | $1,000 loan + cash advance |

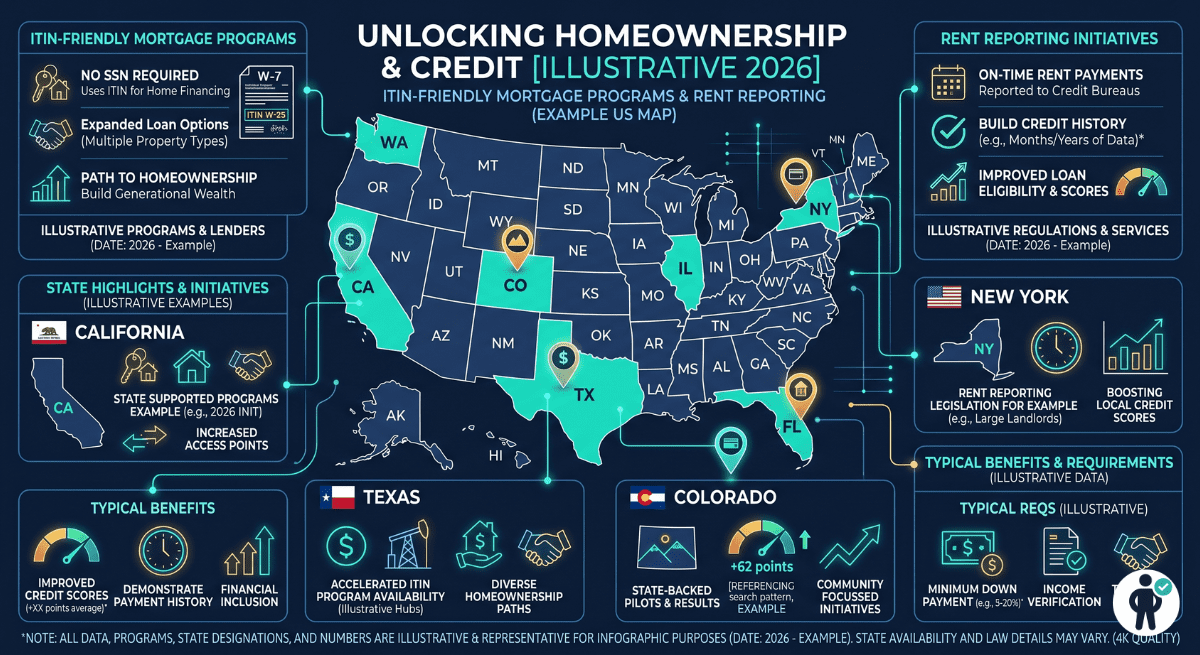

State-Specific Rules for Immigrant Credit Building

Credit building rules and opportunities vary significantly by state. Here are the most important state-specific factors for immigrants in 2026:

California: AB 1466 (effective 2024) requires large landlords (100+ units) to offer tenants the option of having rent reported to at least one credit bureau. If your California landlord hasn’t offered this, you can request it in writing. Additionally, California has the strongest ITIN mortgage programs through the CalHFA (California Housing Finance Agency).

New York: NYC requires landlords with 10+ units to notify tenants of rent reporting options annually. The NY ITIN mortgage market is active — several community banks and credit unions (including Amalgamated Bank and Carver Federal Savings) offer mortgage products specifically designed for ITIN holders.

Texas & Florida: Both states have active ITIN mortgage programs through local credit unions. The Texas ITIN mortgage market is particularly developed — lenders like Self Financial (not the app) and some community banks offer 30-year fixed ITIN mortgages with 20% down. No state income tax in either state makes them popular destinations for immigrant credit builders.

Driver’s License & SSN Exemptions by State: 19 states + DC now issue driver’s licenses to immigrants regardless of immigration status — including California, New York, Illinois, Washington, Colorado, and others. A state-issued ID is typically sufficient to open a bank account, which enables access to most credit-building products.

Common Credit Building Mistakes New Immigrants Make

The difference between immigrants who reach 670 FICO in 12 months and those who stall at 580 for years usually comes down to these avoidable mistakes:

1. Multiple simultaneous applications (the hard inquiry trap). Every time you apply for credit, the lender pulls a hard inquiry that temporarily drops your score 5–10 points. Applying to 5 cards in one week can cost you 25–50 points — the opposite of what you need at the start. Space applications at least 30 days apart and limit yourself to 2 applications in the first 6 months.

2. High credit utilization (>30%). If your secured card has a $200 limit and you charge $180 on it, your utilization is 90% — a severe score penalty. Keep balances below 10% of your credit limit at all times, not just at statement closing. Ideally, charge $20–$30/month and pay it off in full.

3. Ignoring foreign credit import. If you had credit accounts in your home country for 3+ years and you didn’t check Nova Credit, you may be leaving years of positive credit history untapped. Nova Credit works with immigrants from Mexico, India, Australia, Canada, UK, Brazil, Dominican Republic, Kenya, Nigeria, Philippines, and 10+ more countries.

4. Closing your first secured card too early. Your oldest account’s age significantly affects your score. When Capital One upgrades your secured card to unsecured, the account age carries over — this is good. But if you close the card entirely, you lose that history. Never close your first credit card for at least 5 years.

5. Paying minimum balance (not the full balance). Carrying a balance generates interest charges and signals financial stress to scoring models. Always pay the full statement balance by the due date — not just the minimum. Your score doesn’t know whether you carry a balance intentionally or by necessity; it only knows utilization and payment history.

FICO 8 vs VantageScore 4.0 for Immigrants (Which Scores Matter)

There are two major scoring models, and they treat new immigrants differently. Understanding which score is used for which purpose helps you prioritize correctly:

| Score Model | Used For | Min History Required | ITIN Handling |

|---|---|---|---|

| FICO 8 | Mortgages, auto loans, credit cards | 6 months + 1 account | Standard — same as SSN holders |

| FICO 9 | Newer mortgage applications | 6 months + 1 account | Ignores paid collections (immigrant-friendly) |

| VantageScore 3.0 | Apartments, utilities, some auto | 1 month + 1 account | Scores sooner — best for early immigrants |

| VantageScore 4.0 | Apartments (2026 standard), utilities | 1 month + 1 account | Fastest to generate a scoreable file |

For immigrants in months 1–6, VantageScore 4.0 is your most important score — it generates faster, uses less history, and is used by the apartment landlords you need to rent from. After month 6, shift focus to FICO 8 as you start approaching auto loan and credit card territory.

When You’ll Qualify for Major Milestones

Use these FICO score thresholds as target checkpoints. Each milestone unlocks real-world financial opportunities:

Secured utility accounts

Subprime auto loans

Standard auto loans

FHA mortgage eligibility

Better auto rates

Unsecured credit cards

Premium unsecured cards

Best auto loan rates

Frequently Asked Questions

Yes. You can build US credit using an ITIN (Individual Taxpayer Identification Number) issued by the IRS. Several major card issuers — including Capital One, Discover, and OpenSky — accept ITIN in place of an SSN on credit applications. Rent reporting services, credit-builder loans, and Experian Boost all work with ITIN as well. The ITIN path takes slightly longer but leads to the same outcome.

The fastest documented path: (1) Set up Experian Boost on day one to add phone, utilities, and rent to your Experian file — this is instant and free. (2) Apply for the Capital One Quicksilver Secured card (ITIN accepted). (3) Open a Self credit-builder loan at $25/month. (4) Ask a family member to add you as an authorized user on their oldest card. Combining all four simultaneously produces the fastest score growth — many immigrants reach a scoreable 580 VantageScore within 30–45 days and 630+ FICO within 6 months.

Yes, but not all issuers. The three confirmed ITIN-accepting secured cards in 2026 are: Capital One Quicksilver Secured, Discover it Secured, and OpenSky Visa Secured. Do not apply to secured cards that specifically require an SSN — the rejection generates a hard inquiry that temporarily hurts your score with no benefit.

Yes, significantly. Experian Boost is one of the most powerful free tools available to credit-invisible immigrants. By adding phone bills, utilities, streaming subscriptions, and rent payments to your Experian file, many users go from “no score” to a scoreable 550–580 VantageScore in days — with no credit check, no deposit, and no cost. It only affects your Experian file (not Equifax or TransUnion), but it’s an essential first step.

With the strategy in this guide, most immigrants can qualify for a standard apartment (no co-signer required) within 6–9 months, when FICO 8 typically reaches 630–660. If you’re in a hurry, some landlords will accept 3 months of bank statements and a larger security deposit (2–3 months) in lieu of a credit score — ask specifically when viewing apartments. Nova Credit also allows some landlords to directly assess your foreign credit history, bypassing the US score requirement entirely.

Free Immigrant Credit Starter Kit (Downloadable Tools)

We’ve assembled a free downloadable kit to help you execute this guide without tracking everything in your head. The kit includes:

- Credit Building Tracker Spreadsheet — Monthly log of all accounts, balances, utilization ratios, and score tracking across all three bureaus

- Application Timeline Template — Pre-filled 12-month calendar with exact dates to apply for each product, request limit increases, and review upgrade eligibility

- State Resources List — State-by-state guide to ITIN mortgage lenders, rent reporting laws, driver’s license access, and community bank ITIN programs

- Authorized User Request Letter Template — A professional template to send to a family member explaining how to add you as an authorized user without sharing their card

Enter your email to receive the complete kit — credit tracker, application timeline, state resources, and authorized user template. Free, no spam.

Action Plan: Start Building Credit This Week

Every week you wait is a week your credit history isn’t growing. Here is the exact sequence to execute starting today — no overthinking required:

Pull all 3 bureau reports at AnnualCreditReport.com. Set up Experian Boost — add rent, phone, utilities. Check Nova Credit if you have foreign credit history.

Apply for Capital One Quicksilver Secured (ITIN accepted). If no US bank account, apply for OpenSky Visa Secured instead. Apply only one card today.

Open a Self credit-builder loan at $25/month. If you have a Chime account, enable Chime Credit Builder instead (free). Set up autopay immediately.

Set up RentTrack ($6.95/mo) to report rent to all 3 bureaus. Enroll in Credit Karma (free) to track VantageScore weekly. Ask a family member about authorized user status.

Make 1–2 small purchases on your secured card. Pay the full balance before the due date. Keep utilization under 10%. Set a calendar reminder for month 6 upgrade review.

Check FICO score at Experian.com. Apply for second secured card if not done yet (Discover it Secured). Request authorized user addition from family member.

Capital One upgrade review fires automatically. Request credit limit increase. FICO 8 should be 630–660. Begin researching apartments — you’re close to qualifying.

Self loan completes — savings returned. Apply for first unsecured card (Petal 2 or Deserve EDU). FICO 8 target: 670+. Begin apartment applications and auto loan pre-qualification.